#1 Ultimate SSS Retirement Requirements Philippines 2026 (Complete & Easy Guide)

Reaching the end of your professional career should be a time of celebration, relaxation, and peace of mind. After decades of contributing to the Philippine workforce, it is finally time to reap the rewards of your hard work. The Social Security System (SSS) retirement benefit is designed to be your primary financial safety net, ensuring you have a steady stream of income or a substantial lump sum to fund your golden years.

However, claiming your retirement fund is not a magical, automatic process. The SSS will not simply knock on your door with a check the moment you turn 60. You must formally file a claim, and the landscape of government transactions has drastically changed. The SSS is now heavily digitized, enforcing strict online enrollments, bank verifications, and digital identity checks.

If you are unaware of the exact SSS Retirement Requirements Philippines 2026, a single missing document or an unverified bank account can delay your life savings for months. As your definitive guide to Philippine bureaucracy, RequirementPH has built this ultimate, foolproof masterclass. We will walk you through the exact eligibility rules, what to do if your former company went bankrupt, how the new WISP provident fund affects your payout, and how to protect your hard-earned money from online scammers.

Step 1: Determine Your Eligibility (Age and Contributions)

Before you gather your documents, you must first confirm that you are legally allowed to retire under the eyes of the Social Security Act. Your eligibility dictates whether you receive a lifetime monthly pension or a one-time lump sum payment.

The Age Requirement: Optional vs. Mandatory

You cannot file for retirement whenever you feel like it. You must hit specific age milestones:

- Optional Retirement (Age 60 to 64): You can choose to retire as early as 60 years old. However, there is a strict condition: you must be fully separated from employment, and you must have ceased all self-employed or OFW operations. You cannot claim an early retirement benefit while still working a formal corporate job.

- Mandatory / Technical Retirement (Age 65): Once you reach 65, the SSS considers you technically retired regardless of your employment status. Even if you choose to continue working and earning a salary at a private company, you can simultaneously start receiving your SSS retirement benefits.

- Special Exceptions: Underground or surface mineworkers can file for optional retirement at age 50 and mandatory at 60. Racehorse jockeys face mandatory retirement at age 55.

The 120-Month Rule: Pension vs. Lump Sum

Your contribution history determines the type of retirement benefit you will receive:

- Lifetime Monthly Pension: You must have paid a minimum of 120 monthly contributions (equivalent to 10 years) prior to the semester of your retirement.

- Lump Sum Amount: If you reach retirement age but have paid less than 120 contributions (for example, you only have 85 posted contributions), you will not get a monthly pension. The SSS will simply return all the contributions you and your employers paid into the system, plus earned interest, in one single payment. Your account is then permanently closed.

The Core SSS Retirement Requirements Philippines 2026 Checklist

If you meet the age and contribution benchmarks, you are ready to compile your documentary folder. Because the SSS is shifting to a paperless system, many of these will be submitted digitally via the My.SSS portal, but physical copies may be required for branch verifications.

1. Primary Identification and Application Forms

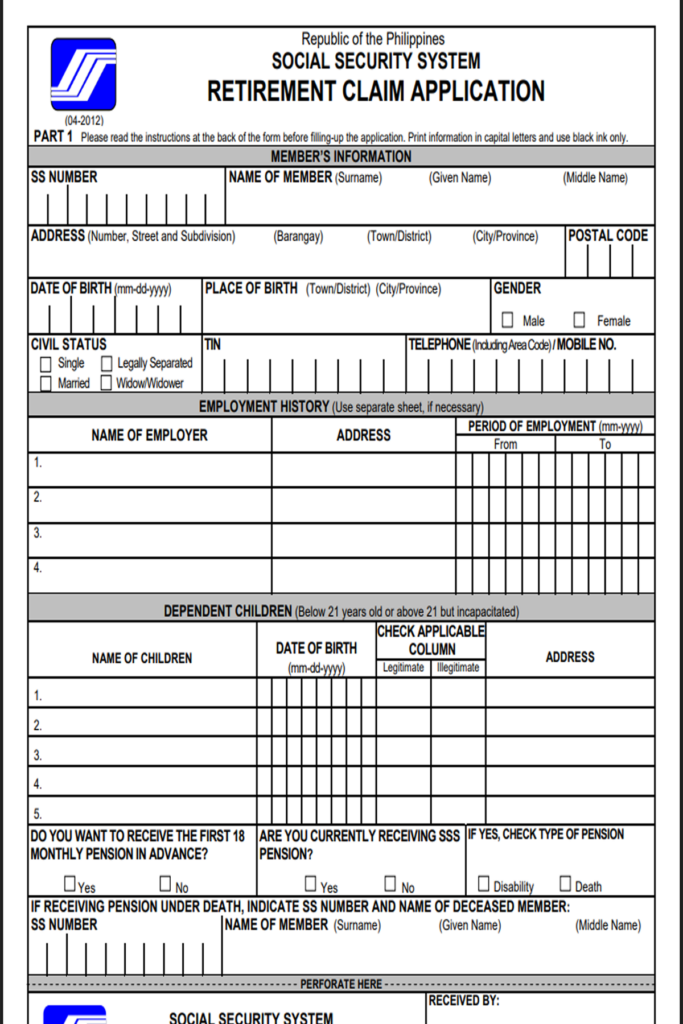

- Retirement Claim Application (DDR-1 Form): If you are filing at a physical branch, this is the master document. If you are filing online, the system generates this electronically.

- Two (2) Valid Identifications: You must present your UMID (Unified Multi-Purpose ID) or PhilSys National ID. If you lack these, you can use a valid Passport, Driver’s License, PRC ID, or Seaman’s Book. Always bring the original cards and clear, back-to-back photocopies.

- Original PSA Birth Certificate: This is critical to legally verify your exact age. If the birthdate on your PSA certificate does not match the birthdate registered in the SSS database, your retirement claim will be suspended until an Affidavit of Discrepancy is filed and resolved.

2. Employment Separation Documents (Crucial for Age 60-64 Retirees)

If you are filing for optional retirement before age 65, the SSS demands undeniable proof that you are no longer working. You must secure:

- Certificate of Separation from Employment: This must be issued and signed by the HR department or authorized signatory of your last employer, indicating the exact effective date of your resignation or retirement.

Troubleshooting: What if your company went bankrupt or closed down?

This is a massive hurdle for many senior citizens. If your previous company no longer exists and you cannot acquire a certificate, you must execute a Notarized Affidavit of Separation from Employment. In this legal document, you must state the name of the company, the approximate date they ceased operations, and swear under oath that you are no longer employed. Submit this affidavit in lieu of the HR certificate.

3. Dependent Documents (For Additional Pension)

If you have minor children (unmarried, unemployed, and below 21 years old), they are entitled to a Dependent’s Pension. This grants an additional 10% of your basic monthly pension or ₱250 per child (whichever is higher), for up to five children. To claim this under your SSS Retirement Requirements Philippines 2026, you need:

- Original PSA Birth Certificates of the dependent children.

- Original PSA Marriage Certificate of the retiring member.

The Mandatory DAEM Registration (How You Actually Get Paid)

The SSS no longer prints physical checks and mails them to your house. In 2026, the disbursement of life savings is strictly digital. Before you even attempt to file your retirement claim, you must successfully complete the Disbursement Account Enrollment Module (DAEM).

This is a non-negotiable step in the SSS Retirement Requirements Philippines 2026 process. You must log into your My.SSS web portal and enroll an active savings account from a PESONet-participating bank, or an upgraded e-wallet like GCash or Maya.

Strict Warning on Bank Accounts: The bank account must be a single account strictly under your exact name. Joint accounts (especially “and/or” accounts with a spouse or child) are heavily scrutinized and almost always rejected for retirement disbursements. The SSS does this to prevent legal complications if the pensioner passes away.

Pro-Tip: Enroll your bank account in the DAEM at least 15 to 30 days before you plan to file for retirement. The SSS evaluation team manually verifies these bank accounts. If your DAEM is still pending approval, the system will completely block you from clicking “Submit” on your retirement application.

The WISP Factor: An Extra Payout for 2026 Retirees

If you are retiring in 2026, there is a massive new variable in your payout: the Workers’ Investment and Savings Program (WISP). Made mandatory in 2021 for members earning above a ₱20,000 Monthly Salary Credit (MSC), the WISP is a separate provident fund that sits on top of your regular pension.

When you complete your SSS Retirement Requirements Philippines 2026 and your claim is approved, your accumulated WISP contributions (plus all tax-free investment dividends earned over the years) will be processed simultaneously. You will have the option to receive your WISP funds as a one-time massive lump sum, or have it added as an annuity to your regular monthly pension, significantly boosting your monthly cash flow.

Making the Big Decision: The 18-Month Advance Option

During the application process, the SSS will present you with a critical financial choice: Do you want your first 18 months of pension paid to you immediately in advance?

- If you choose YES: You will receive a very large lump sum in your bank account shortly after approval. However, you will not receive any monthly pension for the next year and a half. Your regular monthly deposits will only resume on the 19th month of your retirement.

- If you choose NO: You will begin receiving your standard monthly pension immediately on the first month following your retirement date.

Which should you choose? The 18-month advance is excellent if you need immediate capital to build a small business (like a sari-sari store, an apartment rental, or a tricycle boundary business), or if you need to pay off a massive medical debt. However, if you do not have a strict financial plan, taking the advance is risky. Many retirees spend the lump sum in a few months on vacations or giving money to relatives, leaving them completely broke and without a monthly income for the next year and a half.

Post-Retirement Maintenance: The ACOP Rule

Fulfilling your SSS Retirement Requirements Philippines 2026 and getting approved is a huge victory, but you have one ongoing responsibility to keep the money flowing: The Annual Confirmation of Pensioners (ACOP).

To prevent fraud (such as families hiding the death of a retiree to illegally continue withdrawing their pension), the SSS enforces a “Proof of Life” rule. Once a year, usually during your birth month, you must report to your depository bank or an SSS branch to prove you are still alive. If you fail to comply with the ACOP, the SSS will instantly freeze your pension deposits. For bedridden or highly fragile senior citizens, the SSS accommodates home visits or digital video call verifications via Viber or Microsoft Teams.

WARNING: Protect Your Life Savings from Facebook Syndicates

As the ultimate authority on government transactions, we must issue a severe warning regarding the SSS Retirement Requirements Philippines 2026. Because the online application and DAEM enrollment can be highly confusing for senior citizens who are not tech-savvy, a massive syndicate of “Online Fixers” has erupted on Facebook.

These scammers target the elderly, offering to “process your SSS retirement quickly without the hassle” for a fee of ₱500 to ₱1,000.

This is a devastating trap. Do not engage with them.

Filing for retirement is 100% FREE. When a senior citizen hands over their My.SSS username and password, the fixer logs in and changes the enrolled DAEM bank account to their own digital wallet. The fixer then selects the “18-Month Advance” option. When the SSS releases the massive lump sum (often hundreds of thousands of pesos), the money goes straight to the scammer. They immediately block the retiree on Facebook, leaving the senior citizen completely stripped of their life savings and totally helpless.

Always ask a trusted, immediate family member (a son, daughter, or spouse) to assist you with the My.SSS portal. Never, under any circumstances, give your SSS login details to a stranger on social media.

⚠ Important Notice and Disclaimer

RequirementPH is an independent, privately-run educational platform. Our core mission is to simplify complex government transactions and boost the financial literacy of every Filipino worker. We are NOT affiliated, associated, authorized, endorsed by, or in any way officially connected with the Social Security System (SSS) or any government entity.

While we research tirelessly to provide the most accurate SSS Retirement Requirements Philippines 2026 guide, internal protocols, DAEM approval timelines, and exact pension computations are subject to change based on official SSS circulars. For official benefit computations, account troubleshooting, or to submit your retirement claim, please transact directly through the official SSS website or visit your nearest regional branch.

Your Next Steps & Related Guides

Securing your retirement is the final, most crucial step in your professional journey. If you are preparing your documents and need to ensure your digital records are completely pristine before filing, we highly recommend reading our other comprehensive guides: