#1 Ultimate Pag-IBIG Contribution Table 2026 (Updated Rates & Complete Guide)

For decades, the standard deduction for the Home Development Mutual Fund (HDMF), universally known as Pag-IBIG, remained a constant, almost unnoticeable line item on every Filipino worker’s payslip. However, the economic landscape has shifted drastically. To sustain the massive demand for housing loans and to provide higher dividend yields for its members, the agency recently implemented a historic rate hike that effectively doubled the maximum contribution limit.

If you are navigating the workforce in 2026, relying on outdated contribution tables from five years ago is a massive financial mistake. Whether you are an HR manager calculating payroll, a freelancer managing your own voluntary payments, or an employee simply trying to figure out why your take-home pay has changed, understanding the exact mathematics of the Pag-IBIG Contribution Table 2026 is an absolute necessity.

As your definitive authority on Philippine government transactions, RequirementPH has built this foolproof, comprehensive masterclass. We will break down exactly how the new Maximum Fund Salary (MFS) affects your payslip, provide real-world computation examples for different salary brackets, explain the strict laws protecting domestic workers, and teach you how to legally report employers who deduct your money but fail to remit it to the government.

The Big Shift: Understanding the Pag-IBIG Contribution Table 2026 Rate Increase

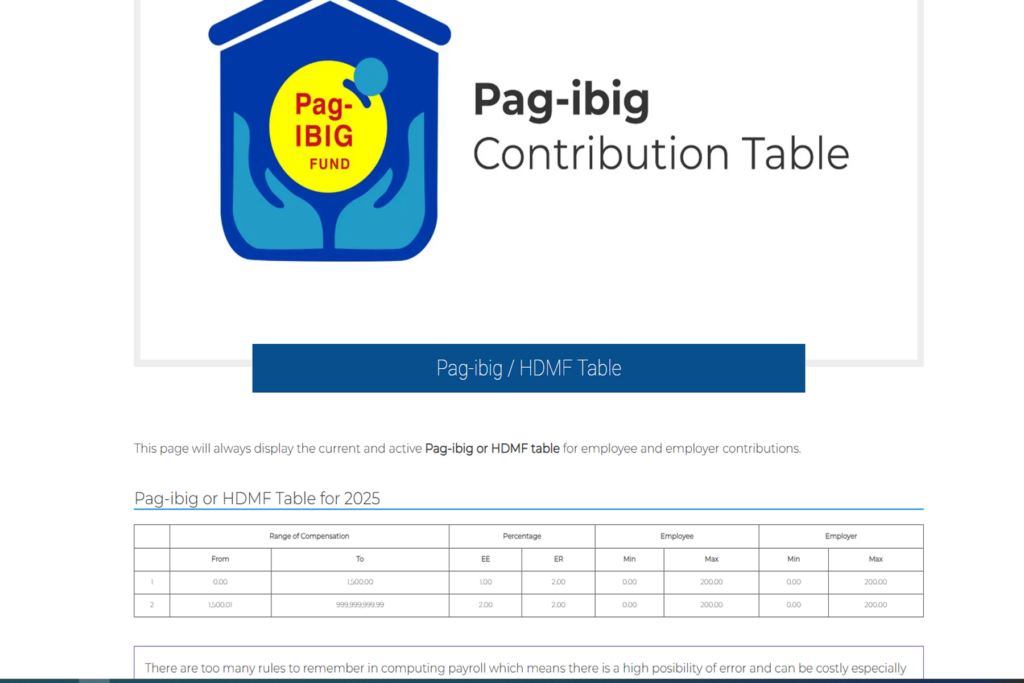

To understand your current deductions, you must understand the history behind the numbers. For nearly forty years, the Pag-IBIG contribution rate was capped based on a Maximum Fund Salary (MFS) of just ₱5,000. This meant that no matter how much money you made—whether you earned ₱15,000 or ₱150,000 a month—the maximum amount deducted from your salary for regular Pag-IBIG savings was only ₱100, matched by an employer counterpart of ₱100.

However, inflation and the rising cost of real estate made this old cap unsustainable. The government needed to increase the fund pool to continue offering low-interest housing loans. Consequently, the Pag-IBIG Fund doubled the Maximum Fund Salary (MFS) limit from ₱5,000 to ₱10,000.

Under the Pag-IBIG Contribution Table 2026, the contribution rate remains at 2%, but because the MFS ceiling is now ₱10,000, the maximum mandatory monthly deduction for employees has doubled to ₱200, with employers mandated to match it with another ₱200. This brings the total monthly mandatory savings to ₱400.

Official Pag-IBIG Contribution Table 2026 (For Employed Members)

For formally employed individuals working in the private sector (covered by SSS) and the government sector (covered by GSIS), the financial responsibility is legally split between the employee and the employer. Here is the official breakdown based on your basic monthly compensation:

- Basic Monthly Salary: ₱1,500 and below

Employee Share: 1.0%

Employer Share: 2.0%

(Note: Very few formal workers fall under this bracket today due to minimum wage laws, but it remains in the charter). - Basic Monthly Salary: Over ₱1,500 up to the ₱10,000 Cap

Employee Share: 2.0%

Employer Share: 2.0%

Because the MFS ceiling is strictly capped at ₱10,000, anyone earning ₱10,000 or above will only ever pay a maximum of ₱200 for their mandatory regular savings.

Real-World Computations: How Much Will Actually Be Deducted?

Looking at percentages can be highly confusing for workers trying to balance their budgets. To ensure your HR department is not overcharging you, let us break down the math using three distinct, real-world salary scenarios under the new Pag-IBIG Contribution Table 2026.

Scenario A: The Minimum Wage Earner

Juan works as a retail clerk in a provincial mall, earning a basic monthly salary of ₱9,000.

- Formula: ₱9,000 x 0.02 (2%) = ₱180.00

- Juan’s Payslip Deduction (Employee Share): ₱180.00

- Employer’s Counterpart (Employer Share): ₱180.00

- Total Monthly Remittance to Pag-IBIG: ₱360.00

Scenario B: The Mid-Level Corporate Worker

Maria is an IT Supervisor in Metro Manila with a basic monthly salary of ₱35,000. Because her salary heavily exceeds the ₱10,000 MFS limit, the computation automatically stops at the ceiling.

- Formula: ₱10,000 (Ceiling limit) x 0.02 (2%) = ₱200.00

- Maria’s Payslip Deduction (Employee Share): ₱200.00

- Employer’s Counterpart (Employer Share): ₱200.00

- Total Monthly Remittance to Pag-IBIG: ₱400.00

Scenario C: The Executive Level Earner

Carlos is a Vice President of a logistics firm earning ₱180,000 a month. Even though he makes six figures, the basic mandatory deduction remains identical to Maria’s.

- Carlos’s Payslip Deduction (Employee Share): ₱200.00

- Employer’s Counterpart (Employer Share): ₱200.00

- Total Monthly Remittance to Pag-IBIG: ₱400.00

Self-Employed, Freelancers, and Voluntary Members

The Philippine gig economy is massive. Millions of Filipinos work as online freelancers, transport network vehicle (TNVS) drivers, online sellers, and independent consultants. If you fall under this category, you are heavily encouraged to maintain your Pag-IBIG account voluntarily.

Because you do not have a corporate employer to subsidize half of your premium, you must shoulder the entire amount yourself.

When you register or update your status via the Virtual Pag-IBIG portal to “Self-Earning Individual,” you essentially pay both the employee and employer share. Since the total mandated savings is ₱400 per month (based on the ₱10,000 MFS cap), self-employed and voluntary members are required to pay the full ₱400.00 every month to keep their accounts active and qualify for future housing loans. You can easily pay this via GCash, Maya, or online banking on a monthly or quarterly basis.

Special Rules for Kasambahays (Domestic Workers)

The government enforces highly specific and protective guidelines for domestic workers under Republic Act 10361, also known as the Kasambahay Law. If you employ a maid, driver, gardener, or yaya, you must follow this specific Pag-IBIG Contribution Table 2026 directive to avoid labor lawsuits.

- If the Kasambahay earns less than ₱5,000 a month: The employer is legally obligated to shoulder the entire Pag-IBIG contribution. You are strictly forbidden from deducting a single peso from their salary.

- If the Kasambahay earns ₱5,000 or more a month: The standard split applies. The employer pays 2% and the Kasambahay pays 2% (via salary deduction).

Can You Contribute More Than the Mandatory ₱200?

A common question among financially savvy Filipinos is: “Can I ask my HR to deduct ₱1,000 instead of ₱200 to boost my savings?”

Yes, you absolutely can. Upgrading your regular Pag-IBIG savings (also known as P1) is an excellent strategy. Unlike standard bank accounts that earn less than 1% interest, Pag-IBIG regular savings historically earn tax-free dividends of around 5% to 6% annually. Furthermore, having a higher accumulated savings value in your regular Pag-IBIG account significantly boosts your approval chances and loanable amount when you apply for a housing loan.

To do this, simply submit a formal letter to your HR department requesting to “Upgrade your Pag-IBIG Regular Savings” and specify the exact amount you want deducted monthly. Note: Even if you increase your personal share to ₱1,000, your employer is only legally required to match the mandatory ₱200 limit.

Alternatively, if you want a purely investment-driven vehicle, you can open a separate Modified Pag-IBIG II (MP2) Savings Account. This is a voluntary, 5-year lock-in savings program that yields even higher dividends (historically between 6% to 8%) and is completely separate from your mandatory regular savings.

How to Verify If Your Employer is Actually Remitting Your Money

One of the most tragic scenarios in the Philippine workforce occurs when an employee finally finds their dream house, applies for a loan, and gets instantly rejected. Why? Because when the evaluator checks the system, they discover that the applicant’s employer has not remitted a single contribution in two years, despite deducting the ₱200 from the employee’s payslip every single month.

This is called remittance fraud (Estafa), and it is a severe criminal offense. Do not wait five years to find out you have been scammed. Here is your action plan:

- Create a Virtual Pag-IBIG Account: Log in to the official Pag-IBIG website and create your online dashboard. This acts as your digital passbook.

- Check Regular Savings: Click on the “Regular Savings” tab. You will see a detailed ledger showing every exact date and amount your employer remitted.

- Demand Reconciliation: If the ledger is blank but your payslips show deductions, immediately email your HR and Payroll department. Give them 5 working days to present the Official Receipts of their bulk remittances.

- Report to Authorities: If the company ignores you, print your portal screenshots and payslips, and proceed to the nearest Pag-IBIG branch. The agency’s legal department will issue a formal demand letter to your employer and file criminal charges if they refuse to comply.

WARNING: Beware of Facebook Scammers and “Discounted Remittance” Fixers

Because some voluntary members and freelancers fall behind on their monthly payments, a massive black market of “Online Fixers” has erupted across Facebook groups and online forums.

You will frequently see posts claiming: “Rush Pag-IBIG Contribution Update! Pay only 50% of your total arrears. Legit transaction, fast posting.”

This is a highly dangerous scam. Do not engage with these syndicates under any circumstances.

Pag-IBIG contribution rates are hard-coded into the national database by law. Absolutely no one can legally offer you a “discount” on your mandatory savings. What these scammers do is take your money, use Photoshop to edit a fake Pag-IBIG Fund Receipt (PFR), and block you on Messenger. When you attempt to apply for a housing loan or calamity loan, the system will show your account in default, and your application will be denied. Always pay your premiums directly through the Virtual Pag-IBIG portal or accredited payment centers like GCash, Maya, and major banks.

⚠ Important Notice and Disclaimer

RequirementPH is an independent, privately-run educational platform. Our core mission is to simplify complex government transactions, eradicate bureaucratic confusion, and boost the financial literacy of every Filipino worker. We are NOT affiliated, associated, authorized, endorsed by, or in any way officially connected with the Home Development Mutual Fund (Pag-IBIG Fund) or any government entity.

While we research tirelessly to provide the most accurate, up-to-date guide on the Pag-IBIG Contribution Table 2026, internal premium caps, MFS adjustments, and specific OFW directives are subject to change based on official HDMF circulars. For official billing statements, account troubleshooting, or to report employer remittance fraud, please transact directly through the official Virtual Pag-IBIG website or visit your nearest regional housing branch.

Your Next Steps & Related Guides

Ensuring your Pag-IBIG savings are consistent and updated is the foundation of your future real estate investments. If you are reviewing your payslip deductions or preparing your pre-employment documents for a new job, make sure your entire government portfolio is completely secure by checking out our other highly detailed master guides:

- Pag-IBIG Online Registration and Virtual Dashboard Setup 2026

- The Ultimate Guide to Pag-IBIG Housing Loan Requirements

- Official SSS Contribution Table 2026 (Updated Rates & Computations)

- PhilHealth Contribution Table 2026 (Understanding the 5% Rate)

- The Ultimate Master Checklist for Pre-Employment Documents

- Pag-IBIG Loyalty Card Plus Requirements