#1 Ultimate Pag-IBIG Housing Loan Requirements Philippines 2026 (Complete Guide)

Owning a home is the ultimate Filipino dream. However, with the skyrocketing prices of real estate, inflation, and the incredibly strict approval rates of commercial banks, buying a house in cash is nearly impossible for the average worker. This is exactly why the Home Development Mutual Fund (HDMF) exists. The Pag-IBIG Housing Loan is the most accessible, lowest-interest, and most forgiving financing option available to the Filipino public.

Whether you are a minimum wage earner dreaming of a modest rowhouse, an Overseas Filipino Worker (OFW) building a retirement home in the province, or a young professional buying your first condominium, Pag-IBIG allows you to borrow up to ₱6,000,000 with payment terms stretching up to 30 years.

But there is a catch. Pag-IBIG is fiercely protective of its members’ funds. If you do not meet their strict income algorithms or if you submit incomplete paperwork, your application will be instantly rejected. To guarantee your approval, RequirementPH has built this comprehensive masterclass. We will break down the exact Pag-IBIG Housing Loan Requirements Philippines 2026, teach you how to legally bypass the 24-month contribution rule, explain how to use co-borrowers, and warn you against Facebook real estate scams.

Eligibility: Can You Actually Borrow?

Before you start looking at model houses and paying reservation fees to developers, you must first verify if you are legally eligible to borrow. Thousands of Filipinos lose their non-refundable reservation fees because they realize too late that they do not qualify for a loan.

To be eligible in 2026, you must meet all of the following baseline criteria:

- Age Limit: You must be no more than 65 years old at the date of loan application, and strictly no more than 70 years old upon loan maturity (when the loan is fully paid).

- Active Membership: You must be an active Pag-IBIG member.

- Contribution Rule: You must have remitted at least 24 monthly savings/contributions.

- Clean Record: You must have NO outstanding Pag-IBIG Short-Term Loan (Salary or Calamity Loan) in arrears or default. If you have an existing salary loan, it must be updated and actively being paid.

- No Foreclosure: You must not have an existing Pag-IBIG housing loan that was foreclosed, canceled, or bought back due to default.

The “Lump Sum” Hack for the 24-Month Rule

What if you just started working 5 months ago, but you found the perfect house today? Do you have to wait another 19 months to apply?

No. You can use the Lump Sum payment method. Pag-IBIG allows members to pay the lacking months upfront. If you only have 5 months of contributions, you can go to a Pag-IBIG branch or use the Virtual Pag-IBIG portal to pay the remaining 19 months in a single lump sum. Once that payment is posted to your account, you instantly qualify under the 24-month rule and can apply for your housing loan the very next day.

Core Pag-IBIG Housing Loan Requirements Philippines 2026

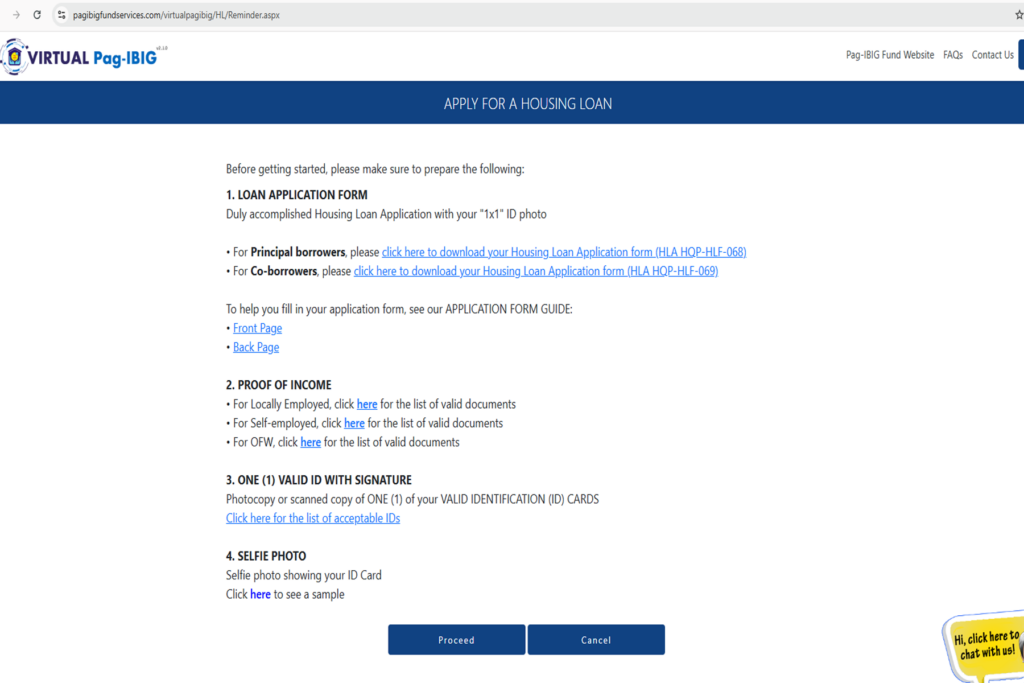

The documentary requirements are heavy because a housing loan is a massive financial transaction. You must organize these files into a neat folder. Missing one signature can cause your folder to be returned to you. The fundamental Pag-IBIG Housing Loan Requirements Philippines 2026 include:

- Housing Loan Application Form (HLAF): Completely filled out with your recent ID photos attached. You can download this from the official website. Ensure there are no erasures.

- Proof of Identity: One (1) valid primary ID (e.g., Passport, PhilSys National ID, UMID, Driver’s License) of the principal borrower, spouse, and any co-borrowers. Bring the original and clear back-to-back photocopies.

- Proof of Income: This is the most heavily scrutinized document. (Detailed in the next section).

Property-Specific Documents (For Retail / Direct Applications)

If you are applying for a “Retail Loan” (meaning you found a house yourself, not through a major developer), you must also provide the technical documents of the property:

- Certified True Copy of the Transfer Certificate of Title (TCT) or Condominium Certificate of Title (CCT).

- Photocopy of the Updated Tax Declaration and Real Estate Tax Receipt.

- Vicinity Map or Sketch of the property.

Pro-Tip: If you are buying a pre-selling house directly from a major real estate developer (like SMDC, Ayala, or Lumina), this is called a “Developer-Assisted Loan.” The developer’s liaison officer will handle all the technical property documents for you. You only need to provide your personal forms and income proofs.

Proof of Income: The Dealbreaker

Pag-IBIG enforces a strict Capacity to Pay rule. By law, your monthly housing loan amortization cannot exceed 35% of your gross monthly income. For example, if your gross salary is ₱30,000 a month, your maximum allowed monthly mortgage payment is roughly ₱10,500. If the house you want requires a ₱15,000 monthly payment, you will be rejected unless you add a co-borrower.

To prove your income, you must provide specific documents based on your employment type:

1. For Locally Employed Workers

- Certificate of Employment and Compensation (COEC) indicating your gross monthly income and all allowances. It must be notarized if there is no company letterhead.

- Latest Income Tax Return (ITR) or BIR Form 2316.

- One (1) month latest authentic payslip signed by your HR.

2. For Overseas Filipino Workers (OFWs)

- Valid Employment Contract authenticated by the DMW/POEA or the Philippine Consulate.

- Certificate of Employment and Compensation (COEC) supported by a photocopy of your employer’s ID or passport.

- If you are currently abroad, you must execute a Special Power of Attorney (SPA) granting a trusted relative in the Philippines the legal right to sign the loan documents on your behalf. The SPA must be consularized by the Philippine Embassy.

3. For Self-Employed and Freelancers

Freelancers and business owners face the highest scrutiny. Pag-IBIG needs concrete proof that your income is stable.

- Latest Income Tax Return (ITR) stamped and received by the BIR.

- Audited Financial Statements for the last 12 months.

- Official DTI Registration or SEC Registration.

- Mayor’s Permit or Business Permit.

- For gig workers (like Upwork/Fiverr freelancers), you must provide printed bank statements for the last 12 months showing a consistent inflow of cash, alongside your contracts.

Co-Borrowing: How to Maximize Your Loan Limit

What happens if your dream house costs ₱2.5 Million, but your salary only qualifies you for a ₱1.2 Million loan? Your solution is to use the Co-Borrower feature.

Pag-IBIG allows you to combine your income with up to two (2) additional co-borrowers (making a total of 3 borrowers on a single property) to increase your total loanable amount. However, you cannot just pick your best friend. Your co-borrowers must be related to you within the second civil degree of consanguinity or affinity.

This means you can only use your spouse, your parents, your children, your siblings, or your parents-in-law. The co-borrower must also pass the exact same Pag-IBIG Housing Loan Requirements Philippines 2026 (they must have 24 months of contributions, good standing, and submit their own proof of income). If one borrower defaults, all borrowers are legally held liable.

Step-by-Step Application Process (Online & Walk-in)

Once your folder is complete, here is how the actual application flows:

- Submit the Application: You can submit your documents physically at a Pag-IBIG housing loan center, or upload them digitally via the Virtual Pag-IBIG portal under the “Apply for Housing Loan” tab.

- Pay the Processing Fee: Upon filing your application, you are required to pay a non-refundable processing fee of ₱1,000.

- Evaluation and CI: Pag-IBIG will conduct a Credit Investigation (CI). They will call your HR department to verify your employment, check your credit history for unpaid credit card debts, and appraise the property you are trying to buy. This takes about 15 to 20 working days.

- Notice of Approval (NOA): If you pass the CI and income algorithms, you will be called to the branch to sign the loan documents and receive your Notice of Approval. At this stage, you will pay the remaining ₱2,000 approval fee.

- Release of Proceeds: Pag-IBIG will release the check directly to the seller or the developer. You will then begin your monthly amortizations exactly one month after the check is released.

WARNING: The Danger of “Pasalo” (Assume Balance) Scams and Fixers

As the ultimate authority on government transactions, we must issue a severe warning regarding real estate scams on Facebook. Because the Pag-IBIG Housing Loan Requirements Philippines 2026 are strict, many buyers look for shortcuts. You will frequently see posts offering “Pasalo” or “Assume Balance” properties.

This is highly dangerous and often illegal.

A “Pasalo” happens when a homeowner can no longer pay their Pag-IBIG loan. They sell the house to you informally; you pay them a cash downpayment, and you agree to continue paying their monthly Pag-IBIG amortization using their name.

If you do this without explicitly transferring the loan legally through Pag-IBIG, you are walking into a trap. Since the loan and the land title are still under the original owner’s name, that original owner can legally claim the house back 10 years later, even after you paid off the entire loan. They can evict you, and you will have zero legal rights to the property.

Furthermore, never engage with “Loan Fixers” who offer to forge fake ITRs or fake Employment Certificates to get your loan approved. Pag-IBIG uses advanced verification systems linked with the BIR. If you are caught submitting a fake ITR, your loan will be permanently canceled, all your payments will be forfeited, and you will face criminal charges for Falsification of Public Documents. Always apply legally.

⚠ Important Notice and Disclaimer

RequirementPH is an independent, privately-run educational platform. Our core mission is to simplify complex government transactions, eradicate bureaucratic confusion, and boost the financial literacy of every Filipino. We are NOT affiliated, associated, authorized, endorsed by, or in any way officially connected with the Home Development Mutual Fund (Pag-IBIG Fund) or any government entity.

While we research tirelessly to provide the most accurate, up-to-date guide on the Pag-IBIG Housing Loan Requirements Philippines 2026 process, internal credit algorithms, interest rates, and loan processing timelines are subject to change based on official HDMF directives. For official loan computations, property appraisal disputes, or application status updates, please transact directly through the official Virtual Pag-IBIG website or visit your nearest regional housing branch.

Your Next Steps & Related Guides

Securing a housing loan requires your government records to be absolutely pristine. If you need to update your membership or check your existing contributions before applying for your dream home, check out our other highly detailed master guides: